Proper wealth management extends far beyond earning and saving money. It involves strategic planning for how your assets will be protected, managed, and distributed—during your lifetime, should you become incapacitated, and after your death. In Kenya, two primary legal mechanisms exist for accomplishing these objectives: trusts and wills. While both serve important estate planning functions, they operate according to fundamentally different principles and offer distinct advantages and disadvantages. This comprehensive article explores how to manage wealth through trusts in Kenya, examining their setup, benefits, drawbacks, incapacity provisions, and critical differences from wills.

Understanding the Fundamental Concept of a Trust

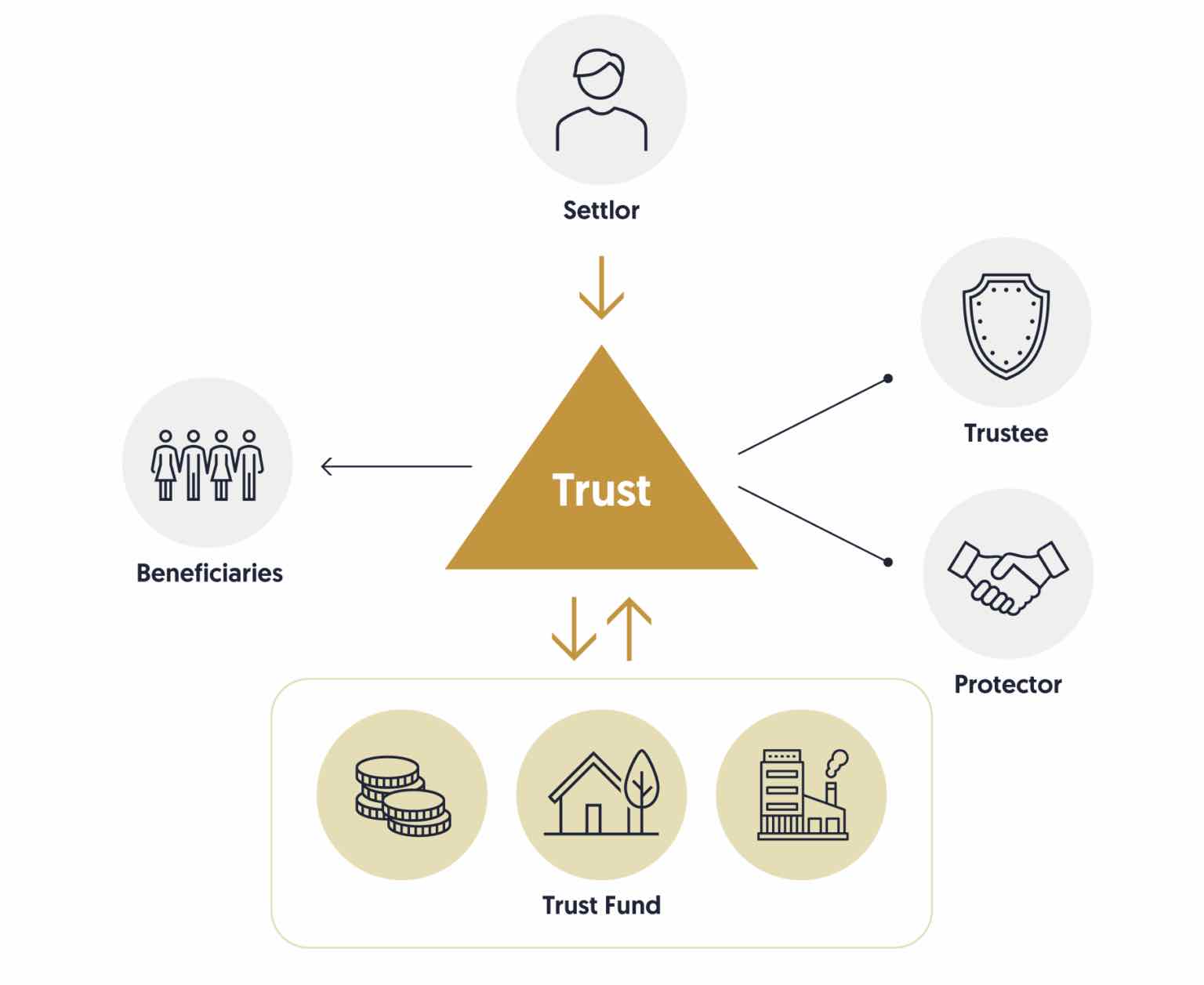

A trust is a legal arrangement in which a person (called the settlor or grantor) transfers ownership of assets to one or more trustees, who are legally bound to hold, manage, and distribute those assets exclusively for the benefit of designated beneficiaries. This arrangement creates a relationship governed by specific legal duties and powers outlined in a written document called the trust deed.

The trust itself becomes a separate legal entity with its own legal personality, capable of owning property, opening bank accounts, entering contracts, and conducting business in its own name. This distinction from individual ownership proves critical to understanding why trusts function so differently from wills in wealth management.

Key Parties in a Trust

The Settlor (Grantor): The person who creates the trust and transfers assets into it. The settlor determines the trust's objectives, selects trustees and beneficiaries, and establishes the terms governing asset management and distribution. A settlor can also be a beneficiary of their own trust, receiving benefits while assets are being managed.

The Trustee(s): The person or entity (typically an individual, corporate trustee, or professional firm) appointed to hold legal title to the trust assets and manage them according to the trust deed's terms. Trustees have fiduciary duties—they must act in the beneficiaries' best interests, manage assets prudently, avoid conflicts of interest, and maintain accurate records. The trustee stands in a position of trust, with potentially significant personal liability for breaches.

The Beneficiaries: The individuals or entities for whose benefit the trustee manages the trust assets. Beneficiaries may be family members, friends, charitable organizations, or other entities. A trust may have multiple beneficiaries with different interests—some may receive income while others receive capital only upon specific conditions.

The Enforcer (Optional): A relatively new role under recent amendments to Kenyan trust law, an enforcer monitors trust administration and ensures trustees comply with trust terms. The enforcer can report financial breaches and require remedial action or legal proceedings against trustees if needed. While not mandatory, enforcers provide an additional layer of accountability and transparency.

How Trusts Are Created and Established in Kenya

Setting up a trust in Kenya involves a series of deliberate steps, each essential to ensuring the trust is legally valid, tax-compliant, and operationally effective.

Step 1: Define Trust Objectives

Before any legal documentation is prepared, the settlor must clearly articulate the trust's purpose. Is the trust intended primarily for:

- Asset protection from creditors or legal claims?

- Succession planning to transfer wealth across generations?

- Tax efficiency through strategic asset structuring?

- Business continuity ensuring enterprises survive the owner's death or incapacity?

- Provision for beneficiaries with special needs or financial vulnerabilities?

- Charitable giving while maintaining family benefits?

- Management of assets during incapacity?

Clear objectives guide all subsequent decisions about trust structure, beneficiary provisions, and trustee powers.

Step 2: Choose the Appropriate Trust Type

Kenya recognizes three categories of trusts under the Trustees (Perpetual Succession) Act (Cap. 164):

Family Trusts: Established for wealth management, asset protection, and succession planning within family contexts. Family trusts are by far the most common type for personal estate planning.

Charitable Trusts: Established exclusively for public benefit purposes including poverty relief, education advancement, health services, environmental protection, human rights advancement, or other purposes beneficial to the general public. Charitable trusts receive preferential tax treatment in recognition of their public benefit purposes.

Non-Charitable Trusts: Established for specific, lawful purposes not falling within family or charitable categories. These might include pension trusts, provident funds, or trusts for other specific objectives.

Additionally, trusts can be further classified as:

Revocable Trusts: Trusts that the settlor can alter, amend, or terminate during their lifetime. However, under recent amendments to Kenyan law, all trusts are deemed irrevocable upon the settlor's death unless the trust deed contains an express power of revocation exercised during the settlor's lifetime.

Irrevocable Trusts: Trusts that cannot be amended or modified after creation except by consent of all beneficiaries or court order. Irrevocable trusts offer greater asset protection and may provide tax advantages but sacrifice flexibility.

Living Trusts: Trusts created during the settlor's lifetime and becoming operational immediately. The settlor can serve as the initial trustee while living and name a successor trustee to assume management upon incapacity or death.

Testamentary Trusts: Trusts created within a will that take effect only upon the testator's death. While useful in certain circumstances, testamentary trusts are subject to probate, negating one of the primary advantages of trust-based planning.

Discretionary Trusts: Trusts where beneficiaries and benefits are ascertainable only through criteria outlined in the trust deed or at the trustee's discretion. Discretionary trusts offer flexibility in distributions but require careful documentation.

Step 3: Select Trustees

Selecting appropriate trustees represents one of the most critical decisions in trust establishment. Trustees must possess:

- Financial sophistication and understanding of investment management

- Integrity and trustworthiness

- Ability to remain neutral among competing beneficiary interests

- Commitment to maintain confidentiality and manage trust administration

- Knowledge of Kenyan trust law and fiduciary obligations

Trustees may be:

- Individual Family Members: Trusted family members serving without compensation or for reasonable fees. Advantages include knowledge of family circumstances and reduced costs. Disadvantages include potential conflicts when distributing to some family members while withholding from others, limited professional expertise, and trustee burnout.

- Multiple Co-Trustees: Two or more trustees serving together, providing checks and balances. Co-trustees can bring diverse expertise and reduce individual burden but require agreement on all decisions, potentially slowing trust operations.

- Professional Corporate Trustees: Banks, trust companies, or private trustee firms providing professional management. Advantages include expertise, permanence, objectivity, and professional administration. Disadvantages include higher costs (typically 1-2% annually of trust assets) and less personal understanding of family dynamics.

- Hybrid Arrangements: Combination of family trustees and professional advisors, or family trustees supervised by a professional enforcer, balancing personal involvement with professional oversight.

Step 4: Identify Beneficiaries and Their Interests

The trust deed must clearly identify:

- Primary Beneficiaries: Those who receive distributions during the trust's initial term

- Contingent Beneficiaries: Those who receive distributions if primary beneficiaries predecease or circumstances change

- Remainder Beneficiaries: Those who receive the trust's capital upon termination

- Distribution Terms: Whether beneficiaries receive income, capital, or both; whether distributions are mandatory, discretionary, or conditional

Clarity regarding beneficiary interests prevents future disputes and ensures trustee understanding of their obligations.

Step 5: Identify and Document Trust Assets

The settlor must compile a detailed inventory of assets to be transferred into the trust, which may include:

Real Property: Residential land, commercial property, agricultural land, buildings, and structures. Land must be formally transferred into the trustees' names under the Land Registration Act.

Financial Assets: Bank accounts, investment accounts, stocks, bonds, unit trusts, money market funds, and other securities.

Business Interests: Shares in companies (listed or unlisted), partnership interests, sole proprietorship businesses, or other business entities.

Intellectual Property: Copyrights, patents, trademarks, domain names, or other intangible property.

Personal Property: Vehicles, jewelry, artwork, antiques, collectibles, or other movable assets.

Retirement Benefits: Pension benefits, provident funds, or employment benefits that can be designated to the trust.

Each asset class requires appropriate legal transfer documentation. Real property transfers must be registered at the Land Registry in the trustees' names. Financial assets require account transfers and beneficiary designation changes. Business ownership documents must be formally assigned. Incomplete or improperly executed asset transfers represent one of the most common causes of trust problems.

Step 6: Draft the Trust Deed

The trust deed is the governing document that formalizes the entire trust arrangement. Unlike wills—which are often standardized—trust deeds must be carefully customized to the settlor's unique circumstances, objectives, and family situation.

The trust deed should include:

Identification of Parties: Full legal names and identification details of the settlor, trustees, beneficiaries, and any enforcer or protector.

Trust Objectives: Clear statement of the trust's purpose and the settlor's intentions.

Trust Property: Detailed description of assets being transferred and provisions for adding assets to the trust during the settlor's lifetime or upon death.

Beneficiaries and Their Interests: Clear identification of who benefits, under what circumstances, and in what proportions.

Trustee Powers and Duties: Express authority for trustees to invest, reinvest, sell, purchase, lease, and manage trust property; power to employ agents and advisors; power to distribute income and capital; duty to maintain records and provide accountings.

Distribution Provisions: Whether distributions are mandatory or discretionary; timing of distributions (regular income, lump sums upon specified events, or at trustee discretion); conditions on distributions (age attainment, educational completion, marriage, etc.); provisions for beneficiary hardship or special needs.

Succession of Trustees: Procedure for appointing successor trustees if the initial trustee dies, resigns, becomes incapacitated, or is removed.

Amendment and Termination Provisions: Whether and how the trust can be amended; whether the settlor retains power to revoke or whether the trust is irrevocable; conditions for trust termination.

Tax Provisions: Tax planning objectives and trustee authority regarding tax matters.

Dispute Resolution: Procedures for resolving beneficiary disputes or trustee disagreements.

Special Provisions: Any unique arrangements such as provisions for minors, spendthrift provisions (restricting beneficiary control over their interests), provisions for beneficiaries with special needs or substance abuse issues, or specific instructions for asset management.

Professional drafting by an experienced trusts lawyer is essential. Standard templates or generic trust documents frequently fail to achieve the settlor's objectives and create foreseeable legal problems. Custom drafting costs more initially but prevents expensive mistakes later.

Step 7: Execute the Trust Deed

Once drafted, the trust deed must be properly executed (signed and witnessed) by:

- The settlor

- All trustees (demonstrating their acceptance of trustee duties)

- Witnesses (usually two independent witnesses who are not beneficiaries or trustees)

Proper execution provides clear evidence of all parties' intentions and legal commitments.

Step 8: Register the Trust

In Kenya, unlike wills which are not registered, trusts must be registered depending on their nature and assets.

Registration with the Lands Registry: If the trust holds immovable property, the trust deed must be registered at the Lands Registry, and land title must be transferred into the trustees' names.

Registration with the Registrar of Documents: Under the Registration of Documents Act (Cap. 285), the trust deed may require registration, particularly if holding significant assets or if the deed affects property rights.

KRA PIN Application: The trust must obtain a Kenya Revenue Authority (KRA) Personal Identification Number (PIN) to transact business, open bank accounts, and ensure tax compliance.

Bank Account Establishment: Most banks require certified copies of the trust deed, trustee identification, and the KRA PIN to open trust accounts.

Stamp Duty: The trust deed must be assessed and stamped at the appropriate registry, with stamp duty payable based on the trust's value.

Step 9: Transfer Assets into the Trust

Mere documentation of assets intended for the trust is insufficient. Assets must be formally transferred into the trustees' legal ownership. This critical step is frequently neglected, leaving assets outside the trust despite intentions to the contrary.

Real Property Transfer: Land must be formally transferred to the trustees under the Land Registration Act, requiring:

- Deed of transfer drafted and executed

- Stamp duty paid

- Transfer application submitted to the Lands Registry with all required documentation

- New certificates of title issued in trustees' names

Financial Assets Transfer: Bank accounts and investments must be re-titled in the trust's name. Financial institutions require trust documentation and identification of trustees.

Business Entity Transfers: Share certificates must be formally assigned to the trust with corresponding company records updated.

Incomplete asset transfers create significant problems. Assets remaining in the settlor's personal name at death will be subject to probate and intestacy law rather than trust distributions, defeating the trust's purposes.

Types of Trusts and Their Specific Applications in Kenya

Revocable Living Trusts

A revocable living trust is established during the settlor's lifetime and can be modified or revoked by the settlor during their lifetime. Upon the settlor's death, the trust becomes irrevocable (unless the trust deed specifically retained revocation power for beneficiaries or executors).

Characteristics:

- Takes effect immediately upon establishment

- Settlor typically serves as initial trustee or co-trustee

- Settlor retains control of assets during lifetime

- Provides for successor trustee management upon incapacity or death

- Assets avoid probate upon death

Best Used For:

- Primary estate planning mechanism for individuals of substantial means

- Asset management during incapacity

- Privacy in asset distribution

- Blended family situations where beneficiary control is important

- Situations where trust terms may require adjustment

Advantages:

- Maintains control during lifetime

- Provides incapacity management

- Avoids probate

- Private distribution of assets

- Flexible—can be amended during lifetime

Disadvantages:

- Assets in revocable trust remain in settlor's taxable estate

- Does not provide creditor protection if settlor also serves as trustee

- Requires ongoing asset management during lifetime

- May require probate for assets not properly transferred

Irrevocable Trusts

An irrevocable trust cannot be amended or modified after creation except with consent of all beneficiaries or court order. Once assets are transferred, the settlor surrenders control and ownership.

Characteristics:

- Cannot be modified after establishment

- Settlor loses all control of assets

- Assets removed from settlor's taxable estate

- Provides strong creditor protection

Best Used For:

- Asset protection from creditors

- Tax planning for high-net-worth individuals

- Protecting assets from matrimonial claims or family disputes

- Life insurance trusts

- Wealth transfer to next generation while minimizing taxes

Advantages:

- Excellent asset protection

- Tax efficiency for large estates

- Assets removed from taxation

- Creditors cannot reach irrevocable trust assets

Disadvantages:

- Complete loss of settlor control

- Inflexible—cannot modify to changed circumstances

- May trigger gift taxes if income-producing

- Difficult to reverse if circumstances change

Discretionary Trusts

Discretionary trusts give the trustee power to determine which beneficiaries receive distributions and in what amounts, based on criteria in the trust deed or purely at the trustee's discretion.

Characteristics:

- Trustee has discretion in distribution decisions

- Beneficiary interests may be uncertain

- Allows trustee to respond to changing beneficiary circumstances

- Provides flexibility in beneficiary treatment

Best Used For:

- Families with beneficiaries in significantly different circumstances

- Protecting financially immature beneficiaries

- Situations where future beneficiary needs are unpredictable

- Asset protection (beneficiaries cannot force distributions)

Advantages:

- Flexible distribution based on circumstances

- Protects immature or financially irresponsible beneficiaries

- Strong creditor protection

- Allows trustee to favor needy beneficiaries

Disadvantages:

- Uncertainty for beneficiaries about distributions

- Potential for conflict if trustee favors some beneficiaries

- Requires trustee wisdom and impartiality

- Beneficial interests may be difficult to value

Costs and Financial Aspects of Trusts in Kenya

Establishing and maintaining a trust involves various costs that prospective settlors should understand.

Initial Setup Costs

Legal Drafting: Professional lawyers typically charge KShs 20,000 to KShs 100,000+ for trust deed drafting, depending on complexity. Simpler family trusts might cost KShs 20,000-40,000, while complex multi-asset or business trusts might reach KShs 80,000-150,000. This investment in proper drafting is essential—errors in trust documentation create far costlier problems later.

Registration Fees: Trust registration costs include:

- Lands Registry registration for land assets: approximately KShs 1,000-5,000 per property depending on value

- Registrar of Documents fees for trust deed registration: typically KShs 500-2,000

- Land title transfer fees: variable based on property value and registration category

KRA PIN Application: Obtaining KRA PIN is free, though accountants or lawyers may charge KShs 500-2,000 if they handle the application.

Asset Transfer Costs: Formal asset transfers into trust ownership involve:

- Land transfer costs (stamp duty, registration fees, surveyor fees): typically 2-5% of property value

- Financial institution charges for account transfers or beneficiary designation changes: typically KShs 500-5,000 per account

- Business entity assignment costs: variable based on complexity

Total Initial Costs: For a straightforward family trust with a home and some financial assets, expect KShs 50,000-150,000 in total initial setup. Complex trusts with multiple properties or business interests may cost KShs 200,000-500,000+.

Ongoing Administration Costs

Professional Trustee Fees: Corporate trustees typically charge:

- Annual fee of 1-2% of total trust value

- For a KShs 5 million trust, this equals KShs 50,000-100,000 annually

- Plus VAT at 16%

- Total annual cost: KShs 58,000-116,000

Accounting and Tax Compliance: Annual trust tax returns and accounting require:

- Professional accountant fees: KShs 5,000-15,000 annually

- Tax preparation fees: KShs 5,000-10,000 if trust has taxable income

Legal Advice: Periodic legal consultations regarding trust management typically cost KShs 1,000-3,000 per hour, with simple questions requiring 1-2 hours annually.

Trust Administration: Trustee out-of-pocket costs include:

- Beneficiary accountings and reports

- Bank account maintenance fees

- Investment management expenses

- Insurance and property maintenance

- Utilities and property taxes

Annual Compliance Costs: Total annual compliance and administration for an active trust with multiple beneficiaries and significant assets might total KShs 100,000-200,000 annually.

Comparison with Will-Based Planning

Wills have significantly lower upfront costs (KShs 5,000-20,000 for simple wills prepared by lawyers) and no ongoing administration costs while the testator lives. However, upon death, wills trigger probate processes that can cost 2-5% of estate value in legal fees, court costs, and delays spanning 1-3 years or longer.

A KShs 10 million estate going through probate might incur KShs 200,000-500,000 in costs plus years of delay. The same estate in a trust would avoid these probate costs entirely, though the trust required higher upfront investment and ongoing administration costs.

For estates under approximately KShs 3-5 million with simple distributions, will-based planning may be more economical. For larger estates, complex distributions, or significant privacy concerns, trust-based planning generally proves more economical over time despite higher upfront costs.

Advantages of Wealth Management Through Trusts

Trusts offer numerous significant benefits that make them powerful wealth management tools for appropriate situations.

Avoidance of Probate

One of the most substantial advantages of trusts is complete avoidance of the probate and administration process. Probate is the judicial process through which a will is verified as authentic, the deceased's estate is inventoried and valued, debts and taxes are paid, and remaining assets are distributed according to the will. This process in Kenya is governed by the Law of Succession Act (Cap. 160) and can be lengthy and expensive.

Probate Problems Avoided by Trusts:

- Court fees and judicial administration costs (2-5% of estate value)

- Lengthy delays (typically 1-3 years, sometimes 5+ years for complex estates)

- Detailed public disclosure of all estate assets and beneficiaries

- Vulnerability to creditor claims (probate assets are exposed to estate creditors)

- Potential for will contests and litigation by disgruntled beneficiaries

- Loss of confidentiality as probate proceedings are public record

With a properly funded trust, assets transfer directly to beneficiaries upon the settlor's death without court involvement, delay, or publicity. Beneficiaries receive distributions within weeks rather than years.

Asset Protection from Creditors

Trusts provide significant protection for trust assets from the settlor's creditors, depending on trust type.

For Irrevocable Trusts: Once assets are transferred to an irrevocable trust, they are removed from the settlor's personal ownership and generally beyond reach of creditors. If a creditor obtains a judgment against the settlor, the judgment creditor cannot seize trust assets because the settlor no longer owns them legally.

For Revocable Trusts: Asset protection is more limited if the settlor serves as trustee, since creditors may argue the settlor retains substantial control. However, if a successor trustee manages revocable trust assets, protection is greater.

Specific Examples:

- A healthcare professional facing malpractice litigation can place assets in an irrevocable trust, protecting those assets from malpractice judgments

- A business owner concerned about business liability can separate personal assets from business exposure through trust structuring

- A professional in a litigation-prone field (attorney, architect, engineer) can maintain necessary professional assets while protecting personal wealth

This protection proves essential for high-net-worth individuals, business owners, healthcare providers, and others facing elevated liability exposure.

Privacy and Confidentiality

Wills become public documents during probate, with complete disclosure of:

- All estate assets and their values

- All beneficiaries and their relationships to the deceased

- All debts and liabilities of the deceased

- Specific bequests to individuals

- Distribution amounts to each beneficiary

This public disclosure may expose assets to fraud, expose beneficiaries to unscrupulous solicitation, or reveal family information many prefer to keep private.

Trusts, by contrast, are private documents. Unless contested or involving public property registration, trust contents remain confidential. Beneficiaries' shares, specific gifts, and trust assets remain private knowledge among the settlor, trustees, and beneficiaries.

For families with privacy concerns—whether due to wealth, family dynamics, or security considerations—trust-based planning provides essential confidentiality.

Control Over Asset Distribution

Wills distribute assets directly to named beneficiaries, who then own and control those assets completely. A beneficiary might spend inherited assets unwisely, lose them to creditors, or have them seized in matrimonial disputes.

Trusts allow the settlor to maintain significant control over how and when beneficiaries receive assets, even after the settlor's death:

Age-Based Distribution: Assets might be distributed in stages—perhaps 1/3 at age 25, 1/3 at age 35, and 1/3 at age 45—ensuring young beneficiaries don't receive large sums before financial maturity.

Conditional Distribution: Distributions might be conditioned on achieving specific goals—completing education, establishing a career, maintaining sobriety, or supporting family members.

Spendthrift Provisions: Specific trust language can prevent beneficiaries from assigning their interests to creditors, preventing inherited assets from being seized by beneficiary creditors.

Special Needs Provisions: For beneficiaries with disabilities or special needs, trusts can provide distributions supplementing government benefits without disqualifying beneficiaries from means-tested programs.

Asset Protection for Beneficiaries: Distributions can flow through continuing trusts rather than directly to beneficiaries, protecting inherited assets from beneficiary creditors, divorcing spouses, or poor financial decisions.

Tax Efficiency

Properly structured trusts can provide significant tax advantages:

Estate Tax Planning: While Kenya currently has no estate or inheritance tax, trusts can minimize income tax by distributing income among multiple beneficiaries in lower tax brackets.

Income Splitting: Income generated by trust assets can be distributed to beneficiaries, with each beneficiary paying tax on their respective share at their individual tax rate, potentially at lower rates than if all income remained with the settlor.

Tax-Efficient Distributions: Trustees can strategically time and structure distributions to minimize tax consequences.

Business Succession Planning: For family businesses, trusts can facilitate smooth transitions while managing tax consequences of ownership transfer.

Charitable Giving: Charitable trusts receive preferential tax treatment, allowing donors to achieve philanthropic objectives while optimizing tax positions.

Proper tax planning through trust structures can preserve significantly more wealth for beneficiaries than poorly structured or absent planning.

Continuity of Management

Trusts ensure assets continue to be professionally managed even if the settlor becomes incapacitated or dies.

During Incapacity: If the settlor becomes mentally incompetent due to illness, accident, or age, a successor trustee automatically assumes management responsibilities. There is no need for expensive and time-consuming guardianship or competency proceedings. Assets continue to be managed smoothly according to the trust deed's terms.

Upon Death: The trust document provides immediate direction for successor trustees, who can continue operations without delay. For family businesses, this ensures continuity without disruption.

Professional Management: A professional trustee brings expertise in asset management, investment strategy, and regulatory compliance, potentially achieving better investment returns and risk management than family trustees might accomplish.

Family Harmony and Reduced Conflict

Clear trust documentation reduces family conflict compared to situations where distribution terms are unclear or where disputes arise over the deceased's intentions.

Explicit Terms: A detailed trust deed eliminates ambiguity about the settlor's wishes, reducing opportunity for disagreement or litigation.

Reduced Litigation Risk: While trusts can be contested, the detailed documentation and clear terms make successful challenges less likely than with wills.

Professional Trustee Neutrality: If disputes arise among beneficiaries, a professional trustee provides impartial administration and can mediate disagreements.

Transparent Accounting: Trustees must maintain detailed records and provide accountings to beneficiaries, ensuring transparency and reducing suspicion or distrust.

Disadvantages of Wealth Management Through Trusts

Despite numerous advantages, trusts involve significant disadvantages that must be carefully considered.

Higher Initial Costs

Professional drafting of a proper trust deed typically costs KShs 20,000-100,000+, compared to KShs 5,000-20,000 for a simple will. For modest estates, this higher initial cost may not be justified.

For clients with limited assets, a simple will may provide adequate planning at much lower cost. The advantages of trust-based planning emerge only when the higher initial investment is justified by estate size or complexity.

Ongoing Administration Complexity

Trusts require ongoing administration that wills do not:

Asset Management: The settlor or trustee must actively manage trust assets, including investment decisions, property maintenance, and financial oversight.

Bookkeeping Requirements: Trustees must maintain detailed records of all trust transactions, income, distributions, and expenses.

Annual Tax Returns: Most trusts must file annual tax returns with the Kenya Revenue Authority, requiring accountant preparation.

Beneficiary Accountings: Trustees must periodically provide beneficiaries with detailed accountings of trust performance, distributions, and asset values.

Compliance: Trustees must stay current on trust law changes and ensure compliance with all applicable regulations.

For settlors uncomfortable with administrative detail or those selecting family trustees without financial expertise, this ongoing complexity creates challenges. Professional trustee fees (1-2% annually of trust assets) somewhat mitigate this burden but add significant costs.

Complexity of Asset Transfer

Properly funding a trust requires careful transfer of assets into the trustees' legal ownership. This process is more complex than simply listing assets in a will:

Real Property: Land title transfers require formal deed preparation, stamp duty, registration, and Land Registry processing.

Financial Assets: Bank accounts, investments, and securities must be re-titled in the trust's name, requiring direct contact with each financial institution.

Business Interests: Share certificates and company records must be formally assigned to the trust.

Ongoing Asset Addition: As the settlor's wealth grows, additional assets must be formally transferred into the trust—a process that requires ongoing attention.

Incomplete asset transfer is common, leaving assets outside the trust despite intentions to the contrary. This creates significant problems when assets must pass through probate rather than flowing through the trust. Professional assistance ensures proper transfers but adds to administration complexity and costs.

Loss of Control (Irrevocable Trusts)

With irrevocable trusts, the settlor permanently surrenders control of assets. Once transferred, assets cannot be returned to the settlor, and the trust cannot be modified (except with beneficiary consent or court order).

If circumstances change—family situation changes, financial needs arise, or the settlor's wishes evolve—the settlor cannot modify the irrevocable trust structure. This inflexibility creates problems for settlors whose life circumstances are uncertain or who are not comfortable with permanent commitment.

For younger settlors or those with uncertain futures, revocable trusts provide more flexibility, though they sacrifice some asset protection advantages.

Potential for Trustee Misconduct

Trustees hold significant fiduciary authority over trust assets. While most trustees are honest, trustee misconduct—whether theft, embezzlement, mismanagement, or self-dealing—is a real risk.

Risk Factors:

- Family trustees may be financially unsophisticated

- Family trustees may prioritize their own interests over beneficiary interests

- Professional trustees may engage in conflicts of interest

- Absence of oversight allows misconduct to continue undetected

Mitigation Strategies:

- Appoint multiple co-trustees requiring mutual agreement

- Appoint an independent enforcer to monitor trustee conduct

- Select corporate trustees with professional oversight and bonding

- Include detailed beneficiary accounting and reporting requirements

- Empower beneficiaries to remove trustees for cause

Proper trust structure can minimize trustee misconduct risk, but the risk cannot be entirely eliminated.

Difficulty Modifying Trust Terms

While revocable trusts can be modified during the settlor's lifetime, modification requires formalities including:

- Amended trust deed execution

- Trustee and settlor signatures

- Registration with appropriate authorities if required

- Asset transfer if terms change beneficiary rights

These requirements are more burdensome than simply amending a will. Additionally, after the settlor's death, irrevocable trusts cannot be modified except with all beneficiaries' consent (often impossible to obtain if beneficiaries have conflicting interests) or court order (expensive and difficult to obtain).

Family Conflict Over Trust Administration

While clear trust documentation reduces dispute likelihood, conflicts can still arise:

Trustee vs. Beneficiary Disputes: Beneficiaries may challenge distribution decisions, allege trustee misconduct, or dispute interpretations of trust language.

Beneficiary vs. Beneficiary Disputes: Competing beneficiary interests may create conflict if the trust permits trustee discretion in distributions.

Trustee Succession Disputes: When a trustee dies or resigns, disputes may arise regarding successor trustee appointments.

These disputes, while less public than probate litigation, can be equally damaging to family relationships and equally expensive to resolve through court proceedings.

What Happens to a Trust if the Settlor Becomes Incapacitated

One of the most important advantages of trust-based planning relates to incapacity management. Incapacity—whether through illness, injury, mental incompetence, or age-related cognitive decline—creates significant challenges for individuals without proper advance planning. Trusts address these challenges elegantly.

Automatic Successor Trustee Succession

If the settlor becomes incapacitated, a properly structured trust allows for automatic succession of trustee authority to a named successor trustee, without court involvement or delay.

How This Works: The trust deed names an initial trustee (often the settlor during lifetime) and successor trustees in order of succession. Upon the settlor's incapacity:

- The successor trustee is notified of the settlor's incapacity

- The successor trustee assumes management of trust assets

- Trust assets continue to be managed according to the trust deed's terms

- No court proceedings are necessary

- No guardianship or conservatorship is required

This automatic succession provides seamless management continuation with minimal disruption.

Continuity of Financial Management

During incapacity, the trust's assets continue to be managed for the settlor's benefit and the beneficiaries' benefit according to the trust deed's terms. Bills are paid, investments are managed, property is maintained, and income is distributed—all without court involvement.

This continuity proves essential for:

- Family businesses that must continue operating

- Real property that requires maintenance

- Investment portfolios requiring active management

- Healthcare and living expense payments

Without a trust, incapacitated individuals require guardianship proceedings—expensive, intrusive court processes—or the incapacitated person's assets remain unmanaged.

Avoidance of Guardianship and Conservatorship

In the absence of advance planning through trusts or power of attorney documents, an incapacitated person requires guardianship proceedings. A court must:

- Hold hearings to determine the person is incapacitated

- Appoint a court-chosen guardian or conservator

- Require court approval for significant financial transactions

- Monitor guardian conduct through court oversight

- Require ongoing court filings and accountings

These proceedings are:

- Expensive: Court fees, lawyer fees, and guardian bonds can total tens of thousands of shillings

- Intrusive: Personal and financial information becomes part of public court records

- Disempowering: The incapacitated person loses financial autonomy

- Slow: Proceedings can take months to complete even for straightforward cases

- Burdensome: Guardians must seek court approval for all significant decisions

A properly structured trust completely avoids guardianship proceedings. The successor trustee assumes management authority automatically, and the incapacitated person's affairs continue with privacy and dignity.

Essential Provisions for Incapacity

To ensure smooth management upon incapacity, the trust deed must include:

Definition of Incapacity: Clear criteria for determining when the settlor becomes incapacitated—typically including mental incompetency, inability to manage financial affairs, or physician certification of incapacity.

Successor Trustee Identification: Specific names of successor trustees in order of succession.

Authority to Continue: Express authority for the successor trustee to continue managing trust assets, making investments, and distributing income as provided in the trust deed.

Access to Medical Information: Authorization for the successor trustee to obtain medical information regarding the settlor's condition, enabling informed trustee judgment about incapacity.

Personal Care Provisions: If the trust deed addresses personal care (not strictly trust property management), provisions authorizing successor trustees to arrange healthcare, housing, and other personal care decisions.

Distinction from Power of Attorney

Power of Attorney documents provide an alternative mechanism for incapacity management, specifically authorizing an agent to manage the principal's financial affairs. However, Powers of Attorney:

- Apply only to assets outside any trust structure

- Cease upon the principal's death (unlike trusts which continue)

- Provide no probate avoidance

- Offer no asset protection benefits

- Require ongoing principal assets to remain in personal name

For comprehensive incapacity planning, both a trust and complementary power of attorney documents are ideal—the trust handling substantial assets and ongoing management, while the power of attorney handles incidental assets and personal decisions.

Trusts vs. Wills: Fundamental Differences and Comparison

While both trusts and wills serve estate planning purposes, they operate according to fundamentally different principles and offer distinct advantages and disadvantages.

Timing of Effect

Wills: Take effect only upon the testator's death. During the testator's lifetime, a will is merely a written expression of intentions—it has no legal effect until death occurs. Wills do not provide management of assets during the testator's lifetime or upon incapacity.

Trusts: Take effect immediately upon establishment and execution, during the settlor's lifetime. The trust can manage assets, distribute income, and provide for beneficiaries throughout the settlor's life and continuing after death.

This difference proves critical: wills provide no planning for incapacity during lifetime, while trusts do.

Probate vs. Non-Probate

Wills: Assets in the decedent's personal name at death must be transferred through the probate process as directed by the will. Probate involves:

- Filing the will with the court

- Appointing an executor

- Inventorying and valuing all estate assets

- Notifying creditors and estate heirs

- Paying estate debts and taxes

- Court approval of final distribution

- Transfer of assets to beneficiaries

This process is lengthy (typically 1-3 years), expensive (2-5% of estate value), and completely public.

Trusts: Assets titled in the trust's name pass directly to beneficiaries upon the settlor's death without probate proceedings. Distributions occur quickly (typically weeks) with no court involvement and complete privacy.

This difference alone makes trust-based planning preferable for anyone concerned about estate administration speed, cost, or privacy.

Control and Flexibility

Wills: Once executed, wills cannot control how beneficiaries use inherited assets. A beneficiary receiving a bequest of KShs 1 million can spend, invest, or lose it as they wish. The testator cannot condition distributions or restrict how beneficiaries use inheritance.

Trusts: The settlor retains significant control over how beneficiaries receive assets:

- Distributions can be made in stages (age-based or event-based)

- Distributions can be conditional (upon education completion, sobriety, etc.)

- Spendthrift provisions can protect assets from beneficiary creditors

- Trustee discretion can ensure distributions match beneficiary circumstances

For settlors concerned about beneficiary financial maturity, addiction issues, or creditor vulnerability, trusts provide control that wills cannot offer.

Incapacity Management

Wills: Provide no incapacity planning. If a will's testator becomes incapacitated, the will cannot be accessed or used to manage assets. The incapacitated person's affairs must be handled through guardianship proceedings or power of attorney documents.

Trusts: Automatically provide for incapacity management. Upon the settlor's incapacity, a named successor trustee assumes management authority without court proceedings. This provides seamless continuity and avoids expensive guardianship.

Costs

Initial Costs:

- Wills: KShs 5,000-20,000 for simple wills

- Trusts: KShs 20,000-100,000+ for comprehensive trust planning Wills appear much less expensive initially.

Ongoing Costs:

- Wills: None until death (when probate costs become substantial)

- Trusts: Annual administration costs (professional trustee fees of 1-2% of assets, accounting, and legal advice)

Total Cost Over Time: For substantial estates, trusts typically prove more economical because they avoid probate costs. For modest estates, wills may be more economical.

Privacy and Confidentiality

Wills: Become public documents during probate. All estate assets, beneficiaries, and distributions are disclosed in public court records.

Trusts: Remain private documents. Unless disputed or involving public property registration, trust contents remain confidential among settlor, trustees, and beneficiaries.

For anyone concerned about privacy, trusts provide essential confidentiality that wills cannot offer.

Asset Protection

Wills: Provide no asset protection. Inherited assets pass directly to beneficiaries' personal ownership, exposing those assets to beneficiary creditors, divorcing spouses, or poor financial decisions.

Trusts: Protect inherited assets, especially if distributions flow through continuing trusts rather than directly to beneficiaries. Spendthrift provisions prevent beneficiary creditors from reaching beneficiary interests.

Liability and Fiduciary Duty

Wills: Executors have fiduciary duties to estate creditors, beneficiaries, and the court. Executor liability is significant but limited by the executor's role in estate administration.

Trusts: Trustees have extensive fiduciary duties to beneficiaries, including duties of loyalty, prudence, and full disclosure. Trustee liability is potentially greater than executor liability due to the ongoing nature of trust management and the longer duration of trustee service.

Guardianship of Minor Children

Wills: Allow testators to nominate guardians for minor children. While courts are not bound by parental nominations, courts typically honor well-reasoned parental choices of guardians.

Trusts: Do not explicitly address guardianship; testators must still prepare separate wills (or guardianship designations) naming preferred guardians for minor children. A trust can, however, hold property for minors after the testator's death, providing for management of the minor's inheritance until age of majority.

Succession of Fiduciaries

Wills: Name a single executor, with successor executors named if the primary executor is unable or unwilling to serve.

Trusts: Name successor trustees in specific succession order, with automatic succession upon the prior trustee's death, resignation, or incapacity. This provides clearer succession planning than wills.

Combined Planning: Wills and Trusts Together

Despite the advantages of trusts, most comprehensive estate plans include both trusts and wills, each serving specific functions:

Pour-Over Wills: A will designed specifically to work with a trust, "pouring over" any assets inadvertently left outside the trust into the trust upon the testator's death. This ensures that missed assets are not distributed according to intestacy law but rather flow through the trust structure.

Testamentary Provisions: A will often includes non-property matters that trusts cannot address:

- Guardianship nominations for minor children

- Directives regarding funeral and disposition arrangements

- Specific bequests of personal items

- Instructions regarding digital assets or online accounts

Complementary Functions: The trust handles primary wealth transfer and ongoing management, while the will addresses matters the trust doesn't cover and provides a backup mechanism for inadvertently untransferred assets.

Tax Considerations for Trusts in Kenya

Kenya's tax system treats trusts as taxable entities, with specific provisions governing trust taxation:

Income Tax on Trusts

Trusts must obtain a KRA PIN and file annual income tax returns. Trusts are taxed on:

- Investment income (interest, dividends, capital gains)

- Rental income from trust properties

- Business income if the trust operates a business

- Other taxable income

Beneficiary Taxation

When trustees distribute income or capital to beneficiaries:

- Beneficiaries are taxed on distributed income at their individual rates

- Capital distributions may be non-taxable depending on the nature of the distribution

- Beneficiaries in lower tax brackets may reduce overall tax burden through income splitting

Tax Efficiency Strategies

Properly structured trusts can minimize tax through:

- Distributing income to multiple beneficiaries in lower tax brackets

- Timing distributions to optimize beneficiary tax positions

- Using charitable trust provisions if appropriate

- Strategic investment in tax-efficient vehicles

Professional Advice Essential

Trust tax planning is complex and requires coordination with professional accountants and lawyers. Improper tax planning can result in unexpected tax liabilities and penalties. Professional tax advisors should be engaged early in trust establishment and regularly during ongoing trust management.

Conclusion: Trusts as Sophisticated Wealth Management Tools

Trusts represent powerful, sophisticated tools for wealth management, asset protection, and estate planning in Kenya. When properly established with professional legal guidance, comprehensive asset transfer, and ongoing professional management, trusts can:

- Avoid expensive and lengthy probate proceedings

- Protect assets from creditors and legal claims

- Maintain privacy in asset distribution

- Provide for incapacity management without guardianship

- Ensure professional asset management across generations

- Control how beneficiaries receive inherited assets

- Minimize tax through strategic distribution

- Provide certainty regarding asset disposition

However, trusts are not appropriate for everyone. They require:

- Substantial assets justifying higher upfront costs

- Willingness to invest in professional legal and accounting services

- Commitment to proper asset transfer and ongoing administration

- Trust in named trustees to manage assets responsibly

For individuals of modest means with simple distribution plans, wills may provide adequate and more economical estate planning. For individuals of substantial means, those concerned about asset protection or privacy, or those with complex family or business circumstances, trusts represent the superior estate planning approach.

The decision between trusts and wills—or the combination of both—should be made with the assistance of qualified legal professionals familiar with Kenya's trust law and the individual's specific circumstances, objectives, and family situation. The investment in professional advice upfront pays dividends through decades of effective wealth management and family harmony.

Comments

Post a Comment